Smart Budget Breakdown of a 35-Year-Old Living on $55k a Year

My favorite type of budgeting post to read is budget breakdowns. I love to see the writer’s smart budget breakdown and how people allocate their resources differently.

It’s a fascinating peek into people’s lives and I always walk away with at least one tidbit that I can apply to my own budget.

My friend Chelsea is here to break down her monthly budget. This post is super informative – I hope you love it as much as I do!

I’ve always been proud to be independent, make my own money, and be responsible for my finances. This is my smart budget breakdown for a 35-year-old.

I worked many different part-time jobs while going to university for eight years. I had student loans to help me but needed to make additional funds to support my living expenses.

While going to school, I learned how to live on a low budget to get by as I didn’t have an excess amount of incoming money. Once I started my full-time job and moved up the ladder, it was easy to save as I felt I had a lot of extra money that I didn’t receive previously.

Struggling financially through university helped me prioritize my money and save once the full-time money started flowing my way.

Monthly Smart Budget Breakdown: What I Earn

I earn $3,500 per month (after taxes). Working for a school board allows me to be able to rely on a steady income.

To help me budget on a bi-monthly basis, I use YNAB (You Need A Budget) – a program on the computer that helps me allocate my expenses and savings. It has video tutorials on different ways to save and better understand how to pay off my debt.

My smart budget breakdown for a 35-year-old is in Canadian dollars.

Money I Give Yearly

- $100 to the Sick Kid Foundation

- $135 to provide fifty meals at Hope Mission

- $50 STARS Lottery Alberta

- $50 MS bike ride

I like to help charities every Christmas to provide food for the homeless and help sick kids and their families receive additional support to get through those tough days. Providing emergency medical care to patients as part of the STARS lottery is an important addition.

I support a friend that rides in the MS bike ride fundraiser every year.

It’s a small portion of my funds and offers other people a chance at a better life. Giving is the best gift!

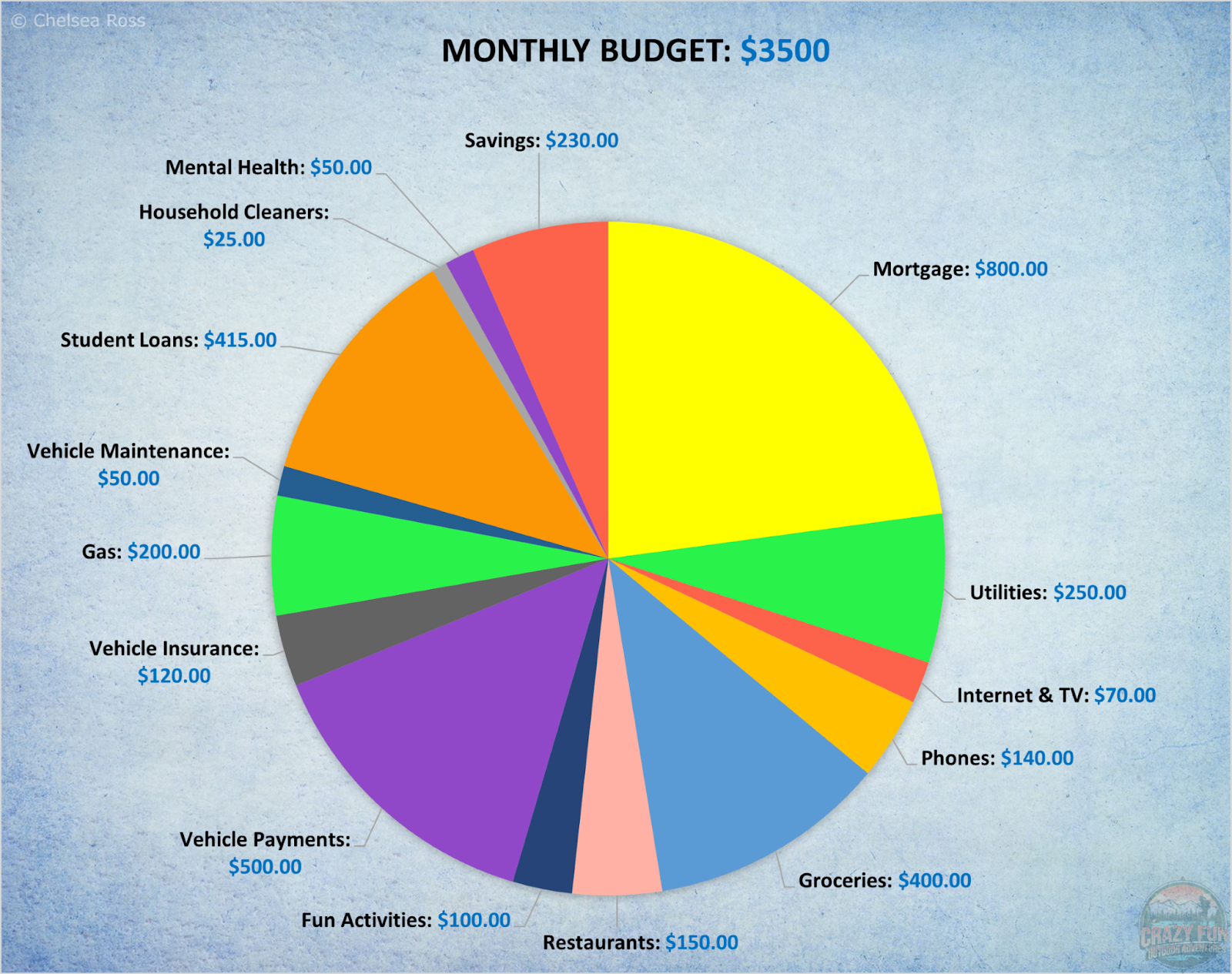

Monthly Smart Budget Breakdown for $3,500 A Month

Mortgage: $800

I contribute eight hundred dollars to our house mortgage (split between my partner and me) based on our incomes. It is for a 1,600 sq ft semi-detached property.

Utilities: $250

My half of water, electricity, and heat come to two hundred fifty dollars every month. This is an expense that has climbed during the last few months of the pandemic and fluctuates month-to-month.

Internet & TV: $70

We called our internet provider and asked them to reduce our monthly payment, resulting in my half being reduced from one hundred dollars to seventy dollars a month.

If you’ve been a long-time customer of an internet provider, it’s worth asking for a rate reduction. If you mention leaving to a different company offering a lower rate, they tend to work out a deal to not lose you as a customer.

It never hurts to inquire. They won’t offer it to you (unless it’s a new package deal) but being smart and asking questions can save you a lot of money!

Phones (1 personal + 1 work phone): $140

Working as a consultant for a school board, I’m required to either have a personal phone where I can also be reached for work or have a work phone for co-workers to reach me.

To maintain my privacy, I chose to get a work phone at an additional cost.

The cost for both phones is one hundred forty dollars, which is expensive – but it’s only until I pay off the built-in payments for my new personal phone. My old phone continuously crashed and had limited storage.

I invested in a more expensive phone resulting in the new phone lasting much longer. In a couple of months, the phone will be paid off, at which point my total for both phones will be closer to one hundred dollars a month.

Groceries: $400

Groceries can get expensive depending on what you buy, but I mostly get fresh food to make home-cooked meals. If I can find sales, I’ll buy packages of frozen fish or frozen chicken stuffed with ham and store them in the freezer.

I make an effort to remind myself to eat the food stashed away in the pantry or the freezer before going back to the grocery store to purchase more items. This allows me to save on costs by preventing expired or stale food from being thrown out.

I bring a grocery list with me and buy needed items or some that are low in stock. That’s instead of getting items when I’m hungry or that don’t need to be replenished.

Baking loaves, cookies, or desserts prevent me from buying expensive unhealthy items at my grocery store.

Restaurants: $150

Every once in a while, it’s nice to treat myself to an expensive supper. I usually keep this for Friday nights after a long work week.

I’m not normally a fan of eating out at fast food places, as it isn’t the healthiest and those twenty-dollar meals add up quickly. I prefer to eat at a sit-down restaurant and order a main meal with a drink and enjoy a pleasant evening out.

This monthly allocation fluctuates. The money is used as a treat but if I don’t use it, I save it for a trip or transfer it towards my vehicle loan balance to pay it off faster.

Allocating one hundred fifty dollars a month allows me not to overspend and to live within my means.

Before having a budget, I used to spend a lot more money eating out and not realizing how quickly it added up. Being sure to include it in a budget breakdown for a 35-year-old can help reduce spending and increase savings.

Fun Activities: $100

It’s great to save money, but it’s also important to provide myself with some self-love (give myself some credit for all the budgeting I’m doing) and budget for some fun in my life! I like to go to the movies, play a round of mini-golf, go bowling or whatever I like.

Fifty to one hundred dollars for a few fun activities every month helps encourage me to keep saving, ensuring a balance between savings and expenses.

If I allocate all my money towards expenses, I would quickly get discouraged (like I have done in the past) not being motivated to pay bills or put money aside.

Balance is key – I need small wins, such as eating out and entertainment in my life, to keep myself happy.

Vehicle Payments: $500

Three years ago I bought myself a 2017 RAV 4 and was paying monthly charges to a bank. It was hard to know the balance since I didn’t have online access to my account.

I needed to call in and wait one hour to talk to a representative; it became a nuisance and consequently, I wouldn’t put money towards it immediately.

Recently, I switched my loan over to my current bank which offered a lower interest rate to pay down the principal more quickly.

I set up automatic bi-weekly withdrawals of two hundred fifty dollars, which was an increase from my previous withdrawal amount at the previous bank.

My reduced balance every month is visible online and allows me to see how much I owe continually. Physically seeing the remaining debt decrease feels awesome!

If I don’t spend other listed expenses in their entirety, I add that money towards my loan payments.

Vehicle Insurance: $120

I pay it yearly but I save it monthly, to ensure that I’m not scrambling at the last minute to find the money. You never know what unexpected expenses can show up a year later.

If I rely on a single month to pay my entire bill I could end up going into debt, which doesn’t help my financial situation. Be smart – save up and once you need to pay, you’ll be happy to have money set aside.

Gas: $200

As a consultant, I need to travel around the city for work and have to make weekly vehicle payments. I have travel expenses partially covered by work, which I use to allocate two hundred dollars towards my expenses.

As long as I do that every paycheck I can easily pay for this expense.

Vehicle Maintenance: $50

I allocate fifty dollars a month for maintenance, such as an oil change, cracks in the windshield, etc. Having the money saved up for when I need it helps me feel less stressed when unexpected expenses suddenly show up.

I change my tires twice a year (from winter to summer and vice versa) to save on the one hundred fifty dollar change fee (which would be an added expense of $300/year). I like to be independent, anything I can do myself is very empowering.

Student Loans: $415

My student loans have automatic withdrawal dates every month, allowing continual payments throughout the year. As long as I save this amount, I’m good to go.

When I made less money, I applied to make smaller student loan payments. Check into that if you’re in this situation.

Household cleaners: $25

I like to save money for shampoo, conditioner, soap as well as additional house cleaners every month. I always seem to need it at unexpected times and don’t necessarily have enough money allocated in my groceries to pay for this expense.

Having a few extra dollars can make a big difference and it can also save you from having to redistribute your entire funds for the month.

Mental health: $50

I made a decision a while ago to dedicate fifty dollars to monthly meditation and self-love classes. This is one of my most important expenses and I make it a priority to save for it.

I’m much happier when I allocate time for my mental health. Self-love and self-investment have made a world of difference in my life. I highly suggest doing the same.

Savings: $230

The extra $230 I have at the end of the month allows me to save for my giving portions, trips throughout the year, and paying off debt. This also acts as an emergency fund, allowing for unexpected expenses should they arise.

I’m also able to save by doing my own renovations and send my medical expenses to my health spending account. I get monthly pension withdrawals to save for my retirement. Most of the time, the cost is free to exercise.

Smart Budget Breakdown for a 35-Year-Old: I Do My Own Renovations

I helped my partner finish our basement, by doing much of the manual labor ourselves. It would have cost three times the price if we’d hired a contractor.

Health Spending Account (HSA)

I contribute to a Health Spending Account with work and in turn, I can pay for contact lenses, glasses, prescriptions (just to name a few) with the additional funds.

It’s a financial saver not having to dig into my finances to cover these costs.

Health Insurance

I have my health insurance deducted from my paycheck, automatically.

Pension

Deciding to work for the school board, allows me to receive a pension. My budget breakdown for a 35-year-old allows me to focus more on my day-to-day expenses instead of solely focusing on saving up for the future.

My current thought process is to pay off my student loans and my loan for my RAV 4 and to add additional funds to my retirement once that’s all paid off.

Smart Budget Breakdown for a 35-Year-Old: Exercise

I exercise outside by hiking or cross-country skiing where it’s free. I have to pay for gas to drive there and back with my vehicle. There isn’t a user fee, which helps to stay fit while not having to pay additional costs.

This is my budget breakdown for a 35-year-old. Balancing my expenses with my savings ensures I pay off debt and live a happy life. It’s important to remember to allocate money for fun activities (movie or bowling) to keep that motivation to save, while still living life to the fullest.

Doing things independently, like changing my own tires or helping with home renovations, helps to save money. Over time, those costs add up and I’m happy to have the additional money saved up in my account.

Author Bio

Chelsea Ross is the creator of Crazy Fun Outdoor Adventures, an outdoor travel blog. She grew up in an outdoorsy family in Canada, hiking, backpacking, kayaking, cross-country skiing, amongst many other activities. Over the years, her experiences traveling around the world have made her knowledgeable to share her expertise with her online community. Being outdoors promotes great physical and mental health. An outdoor lifestyle can be achieved by picking activities close to home and over time broadening your locations, difficulty and length of the adventures.